Did you receive a ‘greeting’ from the tax office? Here’s how to fill out VAT forms without any trouble.

Complete VAT registration number quickly and easily

Frequent changes in legislation often affect the administrative obligations and financial burdens of small private accommodation providers. One such obligation is the recording and payment of VAT on commissions charged by foreign agencies (such as Airbnb, Booking.com, Expedia, etc.), which has prompted numerous reactions since its introduction. Although the majority of small landlords and associations involved in private accommodation advocated for the abolition of this obligation, it has remained in force, and compliance is being monitored with increasing frequency and scrutiny.

To avoid unnecessary disputes with the Tax Administration and potential financial penalties, make sure that all your obligations have been settled. In the following text, we will guide you through the process of completing the VAT form and paying VAT liabilities to the Tax Administration.

Why is it mandatory to pay VAT on the commission?

Private renters often wonder why they are required to pay this type of tax, especially since it is calculated on a service received from abroad. However, private individuals who rent out rooms, beds, apartments, and holiday homes and who are not entered in the VAT register are considered “small taxable persons” in relation to received intermediary services (for example, a private individual renting apartments on the Adriatic is a “small taxable person” with regard to the intermediary service of finding tourists, which is provided to them by a travel agency from another EU Member State or a third country). When “small taxable persons” receive services from taxable persons, such as travel agencies from other EU Member States or third countries, they are required to calculate and pay Croatian VAT on the received services.

VAT Identification Number

Renters who choose to advertise tourist accommodation through one of the foreign portals based in the EU (for example, Booking.com) are required to apply for a VAT identification number at least 15 days before they start using these services.

To apply for a VAT identification number, it is necessary to submit a completed Application for VAT Registration (Form P-PDV) to the competent branch of the Tax Administration according to the place of residence of the private renter to whom the decision on providing services is issued.

*The request can also be submitted through the ePorezna.

A private renter who has been assigned a VAT identification number will not be charged VAT of another EU Member State by a travel agency from that Member State for the provided service. In such a case, the private renter is required to calculate and pay Croatian VAT at a rate of 25% on the amount of the service received from the foreign agency.

A VAT identification number does not need to be requested in the following cases:

- When business is conducted exclusively with taxable persons from third countries that are not EU Member States,

- When cooperating exclusively with Croatian travel agencies,

- When private renters provide accommodation rental services to taxable persons or private individuals from other EU Member States, since the place of taxation is determined according to the location of the property (Republic of Croatia).

Important!

The assignment of a VAT identification number does not mean registration in the VAT system. After being assigned a VAT identification number, private renters remain flat-rate taxpayers (lump-sum taxpayers). Therefore, private renters who are not registered in the VAT register are not entitled to deduct VAT.

Completing and submitting VAT forms

On the value of services received from abroad (for example, commissions charged by foreign platforms), Croatian VAT at a rate of 25% must be calculated and paid by the 20th day of the current month for reservations with a check-out date in the previous month.Whether the service providers are from the EU or from third countries, the principle is essentially the same, but the VAT forms differ. The explanation follows below.

VAT return (PDV form)

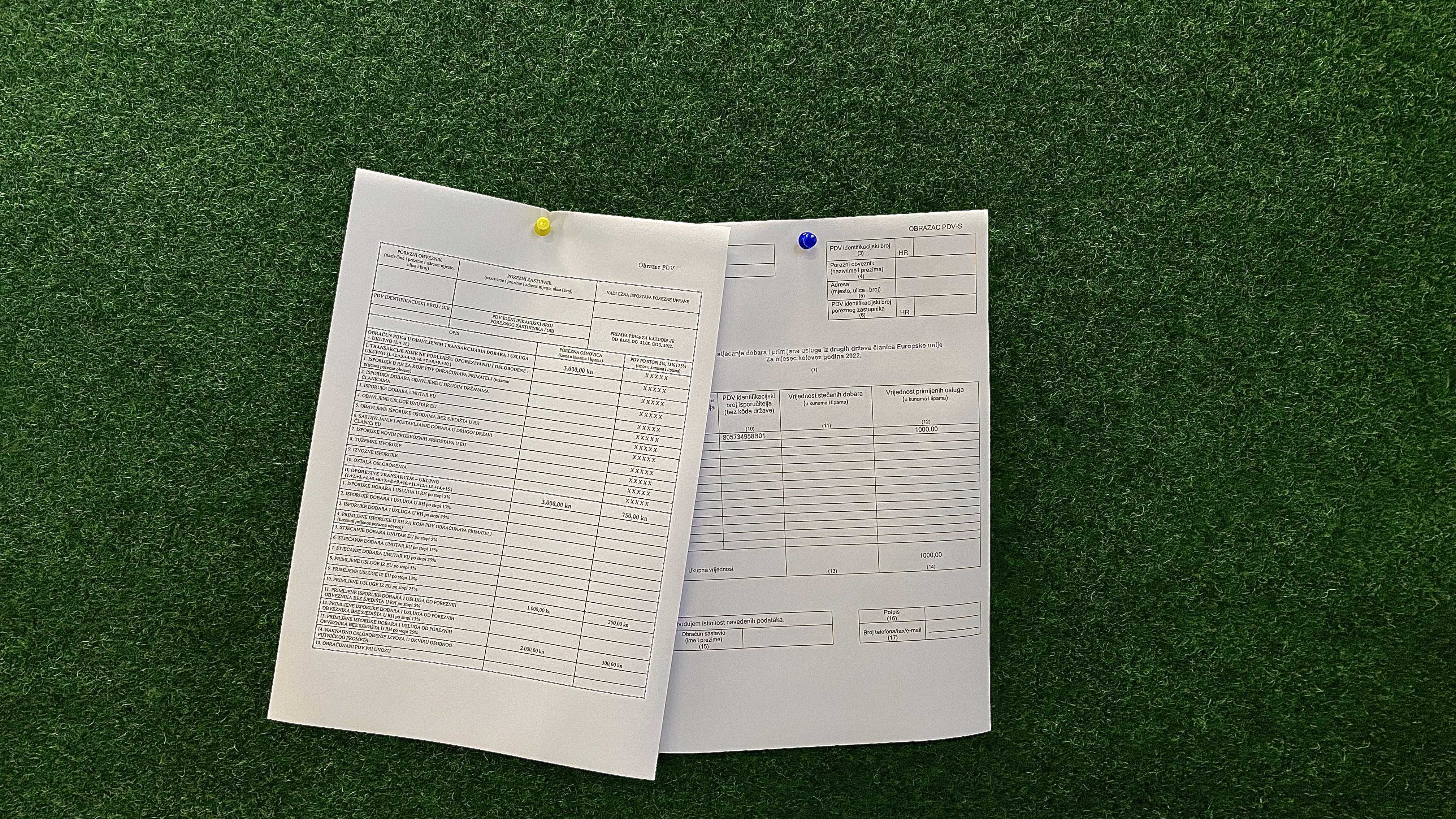

In the VAT return, received intermediary services from taxable persons (for example, foreign agencies) are recorded as follows:

- Row 10– services received from taxable persons from EU Member States

- Row 13– services received from taxable persons from third countries

The second column defines the tax base, which represents the value of the received service, while in the third column VAT must be calculated at a rate of 25%.

HEREyou can find an example of a completed VAT return in the case where the commission of an EU service provider amounts to 1,000, while the commission of a service provider from a third country amounts to 2,000 for services provided in the month of August.

In addition to the amounts related to the calculation, it is necessary to fill in the taxpayer’s information in the first section of the form and to sign the form personally at the bottom.

PDV-S form

The PDV-S form is used to report acquired goods or services received from taxable persons in EU Member States. Services received from third countries are not reported in the PDV-S form.

If a private renter does business only with intermediaries from third countries, they are not required to request or use a VAT identification number; in that case, their OIB (Personal Identification Number) can be used.

Filling out the PDV-S form is fairly simple, and an example can be found HERE.

Note: In the completed form, an example is shown involving a commission from the Booking.com platform, which is based in the Netherlands. Therefore, the country code and the supplier’s VAT identification number (of the Booking.com platform) are included. These details are available online or in the platform’s extranet.

For easier reference, a table listing the headquarters of foreign agencies based on available information can be found below. It is strongly recommended that, before calculating VAT and recording it in the forms, you check the invoices for services received from foreign service providers.

VAT Reporting and Payment

In Croatia, there are three ways to report VAT on services from foreign agencies:

- Directly at a FINA branch,

- By hiring an accounting service that calculates, reports, and pays the VAT obligation on behalf of the renter,

- Self-calculation and reporting of the VAT obligation via the e-Tax system, followed by payment.

When must VAT be paid?

As mentioned earlier, VAT for the previous month must be calculated and the forms submitted by the 20th of the current month, while the payment deadline is by the end of the current month.

According to the instructions published on the Tax Administration website, the calculated VAT should be paid into the state budget as follows:

- Recipient IBAN: HR1210010051863000160

- Model: HR68

- Reference number: 1201–OIB of the taxpayer

Still need help filling out the forms?

Leave all the worry to Litto Agency! Provide us with the necessary documentation, and you will have the completed VAT forms in the shortest possible time.

For a quote, contact us directly at info@litto.agency or +385 911770310.